( ESNUG 496 Item 7 ) -------------------------------------------- [12/15/11]

From: [ A Little Bird ]

Subject: Reader details how SNPS-LAVA dramatically raises SPICE prices

Hi John,

Keep me anonymous.

Here's my rundown of the SPICE Wars pre- and post- LAVA acquisition. I've

included pictures to illustrate the coming changes.

THE PRE-LAVA ACQUISITION SPICE WARS LANDSCAPE

Custom Digital/IO, Memory/Standard Cell Library

Simulators:

- Significant resources went to Synopsys HSPICE/HSIM/XA versus Magma

FineSim war.

- Magma generated $20 to $30 million in FineSim sales/year. They may

actually have sucked their sales pipeline a bit dry and I suspect they

were having trouble sustaining sales at that level.

- Magma left approximately $50 million/year on the table by aggressively

discounting. This impacted Synopsys run rate by an additional $70

million/year in their Fast SPICE franchise. Synopsys' original

franchise was cut from $130 million down to $50 million - $60

million/year.

Environments:

- Solido and MunEDA have grown to provide environments for the memory

and digital territories that are integrated with SPICE vendors.

Characteristics are they run command line batch mode with netlist

input, which is common for these territories. They have 'Switzerland'

positions of being SPICE neutral, providing integrations with all the

simulator vendors and driving simulator license usage across designer

compute farms.

Microwave/RF

Simulators:

- Cadence dominates the RF simulation territory with SpectreRF.

- Cadence at war with BDA AFS and Agilent GoldenGate/ADS.

- National Instruments dominates Microwave territory as a result of

purchasing AWR and are fully capable of taking Agilent head on.

National Instruments is at war with Agilent GoldenGate/ADS.

- Synopsys and Magma will each eventually try to push into this

territory.

Environments:

- Cadence has the dominant environment with ADE, which protects its

SpectreRF simulator from attacks. SpectreRF can be 2x-3x slower than

competitors, but providing the environment buys them time to make

their simulator more competitive. The use of SKILL as an extension to

this environment makes switching cost significant to most customers.

- Solido and MunEDA provide simulation environments for variation

design. Their strategy has been to provide environments integrated

with ADE. They are SPICE neutral, linking to EDA SPICE vendors and

driving simulator license usage across compute farms.

Analog/Mixed-Signal

Simulators:

- Cadence dominates the Analog/Mixed simulation territory with Spectre

and APS. They developed the APS simulator to protect against BDA

attack.

- BDA is growing currently taking approximately $20 million in

sales/year, mostly from Cadence, establishing itself as a real

contender for this space.

- Mentor has plateaued with Eldo doing about $20 million in sales/year.

They have no growth of revenue or new logos. ST is the biggest

signature customer of Eldo.

- Synopsys, Magma and Agilent are trying to push into this territory.

In Synopsys' case, this is also a significant opportunity to help out

their IP business.

Environments:

- Cadence ADE is the dominant environment, by most accounts 70% of the

market, fortressing Spectre/APS from attacks. Spectre/APS can be

2x-3x slower than competitors, but owning the environment gives them

time to make their simulator more competitive.

- Synopsys Custom Designer has largely failed to get market traction by

going head-to-head against Cadence ADE, mostly because they started

with the layout side of the equation instead of developing an

electrical analysis capability.

- Solido and MunEDA provides simulation environment for variation

design. Their strategy has been to provide environments integrated

with ADE. Their SPICE neutrality provides links to all SPICE vendors

and drives simulator license usage across compute farms.

THE POST-LAVA ACQUISITION SPICE WARS CHANGES

Custom Digital/IO, Memory/Standard Cell Library

Simulators:

- Significant resources went to Synopsys HSPICE/HSIM/XA versus Magma

FineSim war.

- Magma generated $20 to $30 million in FineSim sales/year. They may

actually have sucked their sales pipeline a bit dry and I suspect they

were having trouble sustaining sales at that level.

- Magma left approximately $50 million/year on the table by aggressively

discounting. This impacted Synopsys run rate by an additional $70

million/year in their Fast SPICE franchise. Synopsys' original

franchise was cut from $130 million down to $50 million - $60

million/year.

Environments:

- Solido and MunEDA have grown to provide environments for the memory

and digital territories that are integrated with SPICE vendors.

Characteristics are they run command line batch mode with netlist

input, which is common for these territories. They have 'Switzerland'

positions of being SPICE neutral, providing integrations with all the

simulator vendors and driving simulator license usage across designer

compute farms.

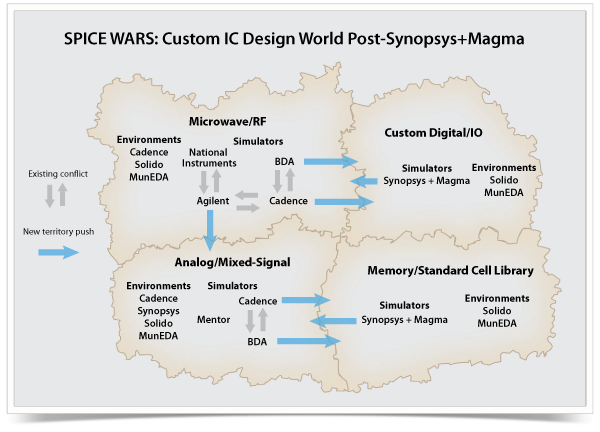

Microwave/RF

Simulators:

- Cadence dominates the RF simulation territory with SpectreRF.

- Cadence at war with BDA AFS and Agilent GoldenGate/ADS.

- National Instruments dominates Microwave territory as a result of

purchasing AWR and are fully capable of taking Agilent head on.

National Instruments is at war with Agilent GoldenGate/ADS.

- Synopsys and Magma will each eventually try to push into this

territory.

Environments:

- Cadence has the dominant environment with ADE, which protects its

SpectreRF simulator from attacks. SpectreRF can be 2x-3x slower than

competitors, but providing the environment buys them time to make

their simulator more competitive. The use of SKILL as an extension to

this environment makes switching cost significant to most customers.

- Solido and MunEDA provide simulation environments for variation

design. Their strategy has been to provide environments integrated

with ADE. They are SPICE neutral, linking to EDA SPICE vendors and

driving simulator license usage across compute farms.

Analog/Mixed-Signal

Simulators:

- Cadence dominates the Analog/Mixed simulation territory with Spectre

and APS. They developed the APS simulator to protect against BDA

attack.

- BDA is growing currently taking approximately $20 million in

sales/year, mostly from Cadence, establishing itself as a real

contender for this space.

- Mentor has plateaued with Eldo doing about $20 million in sales/year.

They have no growth of revenue or new logos. ST is the biggest

signature customer of Eldo.

- Synopsys, Magma and Agilent are trying to push into this territory.

In Synopsys' case, this is also a significant opportunity to help out

their IP business.

Environments:

- Cadence ADE is the dominant environment, by most accounts 70% of the

market, fortressing Spectre/APS from attacks. Spectre/APS can be

2x-3x slower than competitors, but owning the environment gives them

time to make their simulator more competitive.

- Synopsys Custom Designer has largely failed to get market traction by

going head-to-head against Cadence ADE, mostly because they started

with the layout side of the equation instead of developing an

electrical analysis capability.

- Solido and MunEDA provides simulation environment for variation

design. Their strategy has been to provide environments integrated

with ADE. Their SPICE neutrality provides links to all SPICE vendors

and drives simulator license usage across compute farms.

THE POST-LAVA ACQUISITION SPICE WARS CHANGES

- With Synopsys annexing Magma FineSim through the recent acquisition,

Synopsys will monopolize the Custom Digital/IO and Memory/Standard

Cell Library territories. Synopsys will recapture their estimated $70

million/year in lost business to Magma, and with Magma's history of

price cutting and commoditizing now eliminated, the overall market

size for SPICE tools will increase. This definitely fortresses the

former Synopsys franchise with its huge margins to counter the low to

negative margins seen in its IP business.

- FineSim customers will start seeing their Synopsys salespeople after

the close in Q2 2012, who will tell them how their price is going up

dramatically. I suspect there will be very little discounting

considered by Synopsys.

- Disappearance of Magma as the second source SPICE vendor that

customers demand in the Custom Digital/IO and Memory/Standard Cell

Library territories presents a real opportunity for Cadence and BDA to

try to win market share here. Both companies have solid franchises in

the Analog/Mixed Signal/RF territories, and Digital and Memory

characterization is immediately adjacent to both.

- Customers are already calling Cadence and BDA to line up alternatives

to FineSim. Cadence has the resources to extend its current

offerings, and BDA has the capacity, accuracy and precision to compete

in memory and digital.

- Synopsys resources can now be shifted from fighting Magma in its home

turf to pushing into Microwave/RF and Analog/Mixed-Signal territories,

trying to take market share from Cadence, BDA, Agilent, Mentor, and

National Instruments. To achieve this, Synopsys will look to have a

competitive electrical and characterization environment in the next

two years.

- Solido's and MunEDA's SPICE environment for all the territories now

become a key weapon for simulation vendors in the SPICE Wars, to drive

simulator usage and fortress current simulator position, similar to

Cadence's strategy with ADE in Analog/Mixed-Signal territory.

- Cadence and BDA can use Solido's or MunEDA's batch netlist-based

environments to penetrate Custom Digital/IO and Memory/Standard Cell

Library territories. Synopsys can use the Solido's or MunEDA's

ADE-integrated environment to attack into Analog/Mixed-Signal and

Microwave/RF territories. Agilent can use the environments to attack

into Analog/Mixed-Signal territory.

- The new battles will start now but really heat up in Q2 2012. Right

now Magma will look at every deal out there that is renewing in the

next 1 to 3 years and try to convince customers to renew now while

they still can discount. It will be difficult for Synopsys to control

this behavior before the deal is completed.

Finally, there are still risks to the Synopsys acquisition of Magma

actually going through:

- Synopsys may fail to obtain regulatory approval. There is significant

overlap in Synopsys' and Magma's product portfolio, Synopsys will have

a monopoly in a significant chunk of the SPICE market and customers

will be faced with higher prices. FTC usually doesn't stop EDA deals,

but expect some kind of consent decree that allows for opening HSPICE

formats and calls as a way to get the deal done. The asymmetry of

Synopsys' break fee to Magma at only $13 million, versus the $30

million break fee Magma would need to pay Synopsys shows that Synopsys

sees some risk in getting regulatory approval.

- Cadence may still take a run at Magma. Synopsys is paying a 27%

premium of $7.35/share, compared to the $8.40/share Magma's stock was

trading at in July. With the 68.45 million shares Magma has

outstanding, a Cadence bid of $7.85/share would cover the $30 million

break fee Magma would need to pay. This would give Cadence

significant share in the Custom Digital/IO and Memory/Standard Cell

Library territories and keep Synopsys from monopolizing these

territories.

The SPICE Wars are definitely heating up. Expect the BDA simulator and

Solido and MunEDA environments to be acquisition targets as the various

simulator players - Synopsys, Cadence, Mentor, Agilent, National

Instruments - look at having bigger stakes in the SPICE Wars. With Ansys'

recent moves into EDA through their purchase of Apache, they will see this

as an adjacent market and will probably go after Analog/RF first.

Even beyond custom IC, the first half of 2012 will see acquisition activity

that we haven't seen for over five years in EDA.

Furthermore, as custom designers start to look at nanoscale projects, the

traditional simulation markets should start to have more simulator usage

which will drive growth in the overall custom market. Eventually,

cloud-based approaches will find their way into the SPICE wars. The

measured use business model will actually increase simulator usage and

revenue. The only thing standing in the way is the foundry's willingness

to allow their process data and foundry rules to be placed on a cloud.

Interestingly, none of us has any problem with all our credit card and

debit card activity running on a cloud today. It will happen - the

question is when.

- [ A Little Bird ]

- With Synopsys annexing Magma FineSim through the recent acquisition,

Synopsys will monopolize the Custom Digital/IO and Memory/Standard

Cell Library territories. Synopsys will recapture their estimated $70

million/year in lost business to Magma, and with Magma's history of

price cutting and commoditizing now eliminated, the overall market

size for SPICE tools will increase. This definitely fortresses the

former Synopsys franchise with its huge margins to counter the low to

negative margins seen in its IP business.

- FineSim customers will start seeing their Synopsys salespeople after

the close in Q2 2012, who will tell them how their price is going up

dramatically. I suspect there will be very little discounting

considered by Synopsys.

- Disappearance of Magma as the second source SPICE vendor that

customers demand in the Custom Digital/IO and Memory/Standard Cell

Library territories presents a real opportunity for Cadence and BDA to

try to win market share here. Both companies have solid franchises in

the Analog/Mixed Signal/RF territories, and Digital and Memory

characterization is immediately adjacent to both.

- Customers are already calling Cadence and BDA to line up alternatives

to FineSim. Cadence has the resources to extend its current

offerings, and BDA has the capacity, accuracy and precision to compete

in memory and digital.

- Synopsys resources can now be shifted from fighting Magma in its home

turf to pushing into Microwave/RF and Analog/Mixed-Signal territories,

trying to take market share from Cadence, BDA, Agilent, Mentor, and

National Instruments. To achieve this, Synopsys will look to have a

competitive electrical and characterization environment in the next

two years.

- Solido's and MunEDA's SPICE environment for all the territories now

become a key weapon for simulation vendors in the SPICE Wars, to drive

simulator usage and fortress current simulator position, similar to

Cadence's strategy with ADE in Analog/Mixed-Signal territory.

- Cadence and BDA can use Solido's or MunEDA's batch netlist-based

environments to penetrate Custom Digital/IO and Memory/Standard Cell

Library territories. Synopsys can use the Solido's or MunEDA's

ADE-integrated environment to attack into Analog/Mixed-Signal and

Microwave/RF territories. Agilent can use the environments to attack

into Analog/Mixed-Signal territory.

- The new battles will start now but really heat up in Q2 2012. Right

now Magma will look at every deal out there that is renewing in the

next 1 to 3 years and try to convince customers to renew now while

they still can discount. It will be difficult for Synopsys to control

this behavior before the deal is completed.

Finally, there are still risks to the Synopsys acquisition of Magma

actually going through:

- Synopsys may fail to obtain regulatory approval. There is significant

overlap in Synopsys' and Magma's product portfolio, Synopsys will have

a monopoly in a significant chunk of the SPICE market and customers

will be faced with higher prices. FTC usually doesn't stop EDA deals,

but expect some kind of consent decree that allows for opening HSPICE

formats and calls as a way to get the deal done. The asymmetry of

Synopsys' break fee to Magma at only $13 million, versus the $30

million break fee Magma would need to pay Synopsys shows that Synopsys

sees some risk in getting regulatory approval.

- Cadence may still take a run at Magma. Synopsys is paying a 27%

premium of $7.35/share, compared to the $8.40/share Magma's stock was

trading at in July. With the 68.45 million shares Magma has

outstanding, a Cadence bid of $7.85/share would cover the $30 million

break fee Magma would need to pay. This would give Cadence

significant share in the Custom Digital/IO and Memory/Standard Cell

Library territories and keep Synopsys from monopolizing these

territories.

The SPICE Wars are definitely heating up. Expect the BDA simulator and

Solido and MunEDA environments to be acquisition targets as the various

simulator players - Synopsys, Cadence, Mentor, Agilent, National

Instruments - look at having bigger stakes in the SPICE Wars. With Ansys'

recent moves into EDA through their purchase of Apache, they will see this

as an adjacent market and will probably go after Analog/RF first.

Even beyond custom IC, the first half of 2012 will see acquisition activity

that we haven't seen for over five years in EDA.

Furthermore, as custom designers start to look at nanoscale projects, the

traditional simulation markets should start to have more simulator usage

which will drive growth in the overall custom market. Eventually,

cloud-based approaches will find their way into the SPICE wars. The

measured use business model will actually increase simulator usage and

revenue. The only thing standing in the way is the foundry's willingness

to allow their process data and foundry rules to be placed on a cloud.

Interestingly, none of us has any problem with all our credit card and

debit card activity running on a cloud today. It will happen - the

question is when.

- [ A Little Bird ]

Join

Index

Next->Item

|

|